When you open a new bank account today, you don’t just fill out a form-you go through a digital identity check that may already be powered by artificial intelligence. What used to take days, with stacks of paperwork and phone calls to verify your address or employment, now happens in minutes. Behind the scenes, generative AI is quietly rewriting the rules of KYC (Know Your Customer) compliance in retail banking. And it’s not just speeding things up-it’s making compliance smarter, leaner, and far less error-prone.

What KYC Really Means in Retail Banking

KYC isn’t a buzzword. It’s a legal requirement. Every time someone opens a bank account, applies for a loan, or changes their address, the bank must verify their identity and assess their risk. This isn’t just about preventing fraud. It’s about stopping money laundering, terrorist financing, and other illegal activities. In 2025, the average retail bank spends over 20,000 hours per year just on manual KYC reviews. That’s more than 10 full-time employees working nonstop on paperwork, document checks, and cross-referencing databases.

And the cost? A single missed red flag can trigger regulatory fines in the millions. The U.S. Office of the Comptroller of the Currency fined one regional bank $45 million in 2024 for failing to update customer records properly. These aren’t abstract risks. They’re real, measurable, and expensive.

Generative AI Is Doing More Than Automating Forms

Most people think AI in banking means chatbots or automated customer service. But the real breakthrough is in how generative AI handles unstructured data-things like scanned ID cards, handwritten notes from field agents, social media profiles, news articles, and even voice recordings from customer calls.

Take document verification. Before GenAI, a teller or compliance officer had to manually compare a driver’s license with a utility bill, check for signs of tampering, confirm the name matches the application, and then log everything into three different systems. Now, a generative AI model can analyze a photo of a passport, detect if it’s been edited using Photoshop or AI-generated deepfakes, cross-check the issue date against public records, and match the facial features against a selfie taken during onboarding-all in under 12 seconds.

One large U.S.-based bank reported that after deploying GenAI for document analysis, their false rejection rate dropped by 42%. That means fewer honest customers get stuck in limbo because a system flagged their ID as suspicious. At the same time, they caught 37% more fraudulent applications that had slipped through manual checks.

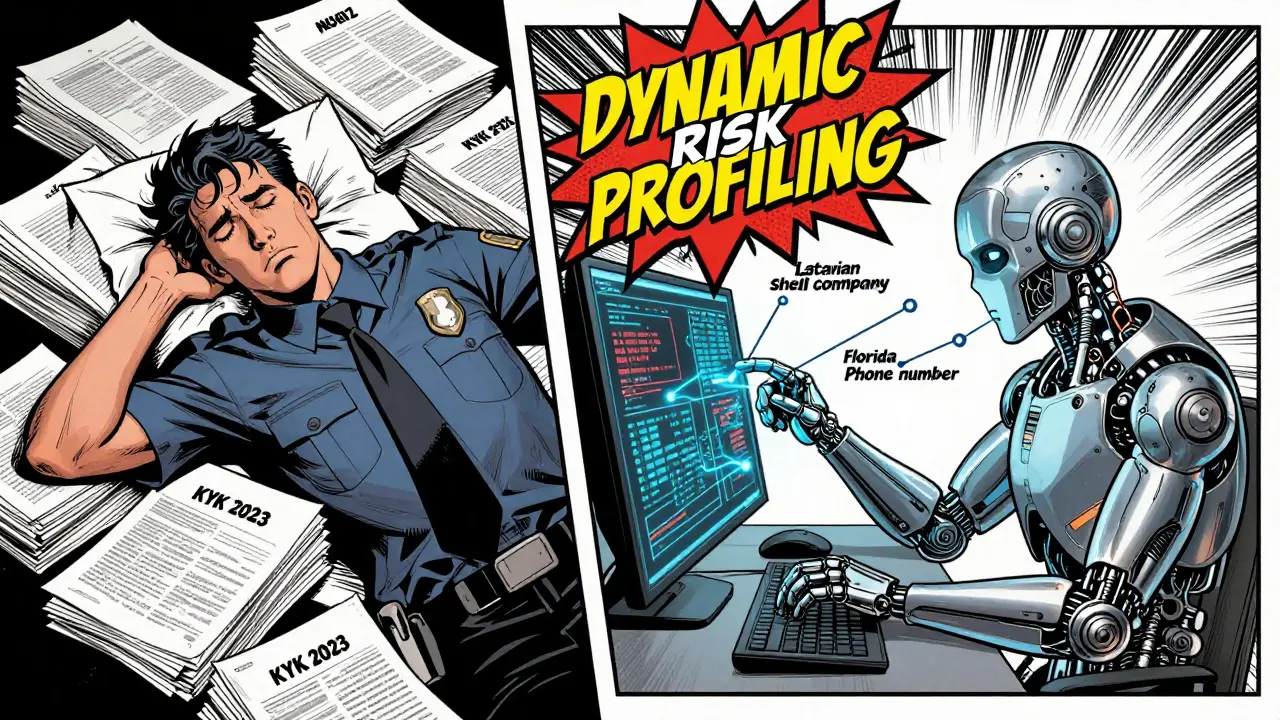

From Reactive to Proactive: How AI Predicts Risk

Traditional KYC systems rely on static rules: “If the customer’s address doesn’t match their ID, flag it.” That’s like using a paper map when Google Maps exists. Generative AI doesn’t just react-it predicts.

By analyzing patterns across millions of customer interactions, AI can spot connections humans would never see. For example:

- A customer in Ohio opens an account, then suddenly starts making small, frequent transfers to a shell company in Latvia.

- Their phone number was previously linked to a suspended account in Florida.

- They’ve been mentioned in a local news article about a Ponzi scheme investigation.

Traditional systems might miss this. GenAI connects the dots in real time, updating risk scores as new data flows in. It doesn’t wait for quarterly reviews. It updates every hour.

This is called dynamic risk profiling. And it’s changing how banks handle ReKYC (recurring KYC). Instead of forcing every customer to re-verify their identity every two years, banks now trigger ReKYC only when risk signals change. A low-risk retiree might never be asked to update their info. A young freelancer with multiple international transactions? They might get a quick video check every six months.

How GenAI Solves the Data Privacy Problem

You might think: “If AI is analyzing my ID, my address, and my transaction history, isn’t that a privacy nightmare?”

Actually, generative AI helps solve that too.

Training AI on real customer data is risky. One breach, and you’re looking at GDPR fines up to 4% of global revenue. So smart banks don’t use real data. They use synthetic data-artificially generated profiles that look and behave like real customers but contain zero personal information.

Think of it like a flight simulator for compliance. Banks train their AI models on thousands of fake identities: a 68-year-old teacher in Kansas with a pension, a freelance photographer in Mexico City, a small business owner in Texas with irregular income. The AI learns what normal looks like. Then it applies that knowledge to real customers.

According to Thoughtworks, banks using synthetic data for training cut their compliance-related data breaches by 63% in 2025. That’s not just a technical win-it’s a trust win. Customers feel safer knowing their real data isn’t being used to train algorithms.

Marketing Compliance: When AI Helps You Stay Legal While Being Personal

Here’s where most people don’t realize AI is working: marketing.

When a bank wants to send you an offer for a personal loan, it can’t just say: “Hey, you’ve been spending a lot on vacations. Here’s a loan!” That’s a violation of fair lending laws. You can’t base financial offers on race, gender, zip code, or spending habits tied to protected categories.

GenAI solves this by creating “compliance filters.” Before an email goes out, the AI scans the offer logic:

- Is this offer based on income, not spending?

- Are we targeting customers who’ve been with us for over 18 months?

- Is the interest rate calculated using a formula that’s consistent across all demographics?

One regional bank in the Midwest used GenAI to audit 87,000 marketing campaigns in Q4 2025. They found 14 campaigns that unintentionally favored customers in higher-income ZIP codes. The AI flagged them, and the team adjusted targeting rules. No lawsuits. No fines. Just better, fairer marketing.

This isn’t about suppressing personalization. It’s about making it legal. And that’s a huge competitive advantage. Customers want tailored offers-but not if they feel like they’re being discriminated against.

Real Results: Numbers That Matter

Let’s cut through the hype. Here’s what actual banks are seeing:

| Metric | Before GenAI | After GenAI Implementation |

|---|---|---|

| KYC onboarding time | 5-7 business days | under 4 hours |

| False positives in fraud detection | 68% | 28% |

| Cost per KYC file | $127 | $98 |

| SAR filing speed | 14 days avg. | 8 days avg. |

| Customer satisfaction (onboarding) | 62% | 89% |

These aren’t lab results. These are numbers from three major U.S. retail banks that scaled GenAI in 2024-2025. One bank even reported a 19% increase in new account openings because customers stopped abandoning applications due to long verification times.

The Hidden Cost of Waiting

Some banks are still stuck in pilot mode. “We’re testing it,” they say. “Let’s see how it works.”

Here’s the problem: GenAI isn’t a feature. It’s infrastructure. The longer you wait, the more you fall behind.

Think of it like mobile banking in 2010. The first banks to launch apps got loyal customers. The ones that waited two years? They lost market share. Now, customers expect fast, seamless onboarding. If your bank still asks you to mail in a notarized form, you’ll leave.

And regulators are catching up. The Federal Reserve and OCC are now asking banks: “What’s your GenAI governance plan?” If you can’t show audit trails, human oversight, and model validation, you’ll be flagged.

Early adopters aren’t just saving money. They’re building trust. They’re reducing risk. And they’re turning compliance from a cost center into a competitive edge.

What’s Next? The Intelligent Compliance Agent

The next leap isn’t just automation-it’s autonomy.

Imagine a compliance agent that doesn’t just process forms but talks to you. You get a message: “Hi, we noticed your last paycheck was from a new employer. Can you confirm your income? We’ll verify it with your payroll provider.” You reply: “Yes, I started at TechNova last month.” The AI checks their payroll system, confirms the data, updates your profile, and closes the file-all without a human touching it.

That’s not science fiction. Moody’s and H2O.ai already have prototypes doing this. These aren’t chatbots. They’re agentic AI systems-teams of AI agents working together, each with a role: one verifies documents, another checks financial history, a third ensures compliance with state laws, and a fourth logs everything for auditors.

And it’s all transparent. You can ask: “Why did you ask me that?” The AI answers in plain language. No jargon. No legalese.

Can generative AI replace human compliance officers?

No-and it shouldn’t. GenAI handles repetitive, high-volume tasks like document checks, data entry, and risk scoring. But humans are still needed for judgment calls: Is that unusual transaction really fraud, or just a one-time overseas gift? Should we escalate this case? Who gets the final approval? The best systems use AI to free up compliance staff for higher-value work, not replace them.

Is generative AI in KYC compliant with GDPR and CCPA?

Yes, if designed right. Leading banks use synthetic data for training and minimize storage of real PII. They also build audit trails, give customers access to their data, and allow opt-outs. The key is transparency: customers should know when AI is involved and how their data is used. Banks that follow these practices are not only compliant-they’re building trust.

What’s the biggest mistake banks make when adopting GenAI for KYC?

Trying to automate everything at once. GenAI works best when you start small: pick one high-cost, high-error process-like document verification-and scale it. Don’t try to overhaul your entire compliance system overnight. Pilot, measure, refine. The goal isn’t speed. It’s accuracy and reliability.

How does GenAI help with marketing compliance?

It stops banks from accidentally violating fair lending laws. Before GenAI, marketing teams would target customers based on spending habits, which could lead to discrimination claims. Now, AI filters ensure offers are based on creditworthiness, tenure, and financial behavior-not ZIP code or gender. This reduces legal risk while still letting banks personalize offers.

Can small banks afford GenAI for KYC?

Yes. Cloud-based GenAI platforms now offer subscription models with no upfront infrastructure costs. A community bank with 50,000 customers can start using KYC automation for under $5,000/month. That’s less than the cost of hiring one full-time compliance officer. The ROI kicks in within six months.

Final Thought: Compliance as a Competitive Advantage

KYC used to be the department everyone avoided. The slow, expensive, frustrating part of banking.

Now, it’s becoming a differentiator. Banks using GenAI aren’t just avoiding fines-they’re offering faster onboarding, fewer errors, and more personalized, trustworthy service. Customers notice. And they stick around.

The future of retail banking isn’t just about better apps or lower fees. It’s about smarter, fairer, and more secure compliance. And generative AI is making that possible-not tomorrow, but today.

Jeanie Watson

February 17, 2026 AT 07:17So now banks are using AI to scan my passport and selfie... cool. But who’s auditing the AI when it flags my grandma’s pension check as ‘suspicious activity’? I’ve seen this movie before - automation doesn’t fix bias, it just makes it faster.

Tom Mikota

February 19, 2026 AT 02:54Let me get this straight: you’re telling me that a machine, trained on synthetic data, can detect a fake ID better than a human who’s seen 10,000 of them? That’s not innovation - that’s a confidence trick. And don’t even get me started on ‘compliance filters’ - because nothing says ‘fair lending’ like an algorithm that’s never seen a real person struggle to pay rent.

Mark Tipton

February 20, 2026 AT 20:19Actually, the numbers here are misleading. The 42% drop in false rejections? That’s only true if you assume the AI’s training data is perfectly representative - which it isn’t. Synthetic data is a statistical mirage. It mimics patterns, not human complexity. For example, a freelance photographer in Mexico City might have irregular income - but the AI doesn’t understand cultural context: maybe they’re paid in cash, or work seasonally, or have family remittances. These aren’t red flags - they’re life. And yet, the system still flags them as ‘high risk.’ The real cost isn’t $127 per file - it’s the erosion of financial inclusion. You’re not making compliance smarter. You’re automating exclusion.

Also, the claim that banks cut breaches by 63% using synthetic data? That’s not because the data is safer - it’s because they’re not storing real PII. But when the AI makes a decision based on synthetic patterns, and then applies it to real people, you’re still risking discrimination. It’s like using a weather model built on Mars to predict rain in Texas. The math looks good. The outcome? Disaster.

And don’t get me started on ‘agentic AI systems.’ That’s not autonomy - it’s opacity. If a customer asks, ‘Why did you ask me that?’ and the AI replies in plain language - fine. But who audits the chain of logic? Who logs the bias? Who’s accountable when the AI denies someone a loan because their phone number was linked to a suspended account in Florida - a suspension they never even knew about? The system isn’t transparent. It’s performative.

And finally - the ROI? Sure, $98 per file sounds great. But what’s the cost of a customer who leaves because they felt surveilled? What’s the brand damage when someone posts on Twitter: ‘My bank used AI to deny me a loan because I live near a school’? Compliance isn’t a cost center. It’s a trust engine. And you’re replacing trust with algorithms that don’t understand trust.

Adithya M

February 22, 2026 AT 06:55Bro, this is the future. Why are we even talking about manual reviews? In India, we’ve been using AI for KYC for over a year now - and it’s cut processing time by 80%. No more waiting weeks. No more calling up relatives to confirm address. Just snap a photo, blink, and done. If you’re still using paper forms, you’re not behind - you’re obsolete.

Jessica McGirt

February 23, 2026 AT 17:59I appreciate how thorough this breakdown is. The shift from reactive to proactive risk profiling is genuinely revolutionary - especially when you consider how many customers are unnecessarily burdened by blanket ReKYC requirements. The use of synthetic data to train models is also a brilliant safeguard for privacy. It’s rare to see such a balanced view of AI’s role in compliance - not as a replacement, but as a tool that empowers both institutions and individuals.

Donald Sullivan

February 24, 2026 AT 15:32Y’all are acting like this is some groundbreaking tech. Nah. Banks have been using bots to dodge regulators for years. Now they just made them look smarter. If your ‘compliance filter’ is just hiding bias behind math, you’re not fixing the system - you’re just making it harder to catch.

Tina van Schelt

February 25, 2026 AT 00:27Imagine walking into a bank and being greeted by a robot that says, ‘Hey, we noticed you’re single, live alone, and haven’t bought anything in six months. Want a loan?’ That’s not personalized - that’s creepy. AI should help, not haunt.

Ronak Khandelwal

February 25, 2026 AT 08:06This is beautiful 🌟 Seriously - AI isn’t here to replace humans, it’s here to help us focus on what matters: dignity, fairness, and connection. When tech lifts the weight of paperwork off people’s shoulders so they can live their lives? That’s not innovation. That’s compassion. 🙌

Jeff Napier

February 26, 2026 AT 18:43GenAI in banking? More like GenAI in propaganda. They say it’s ‘transparent’ - but if you can’t see the code, the training data, or the decision tree, then it’s just a black box with a nice UI. And who controls the black box? Not you. Not me. Some Silicon Valley firm with a patent and a board meeting. This isn’t progress - it’s surrender.